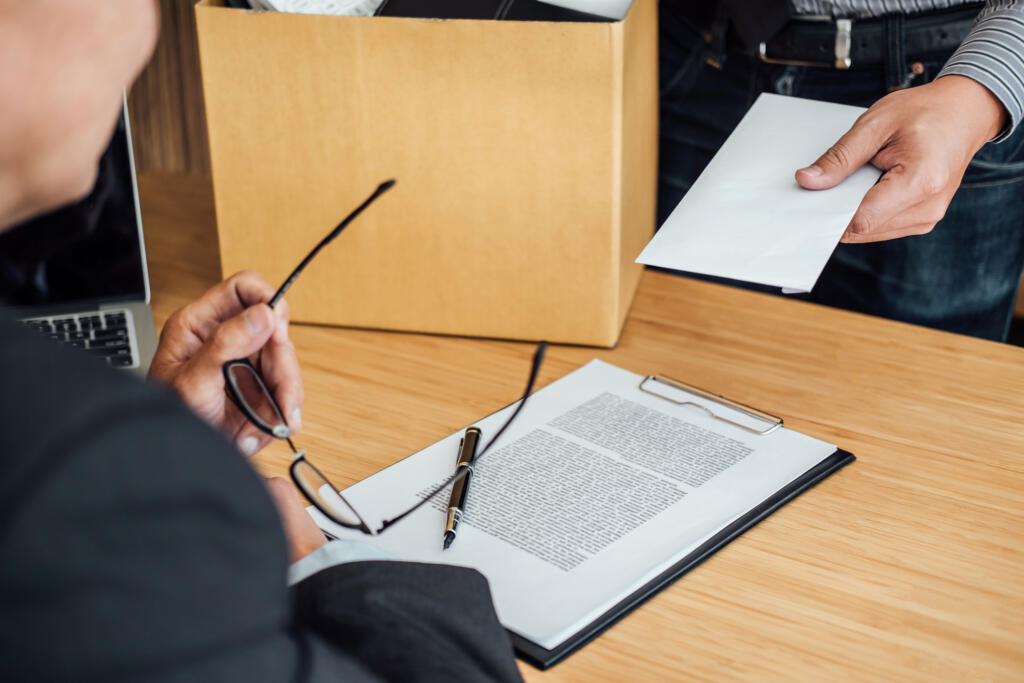

Has your employer given you a settlement agreement? It is not uncommon for settlement agreements to be offered to employees to terminate their employment. What does it mean for you and how should you approach being presented with a settlement agreement?

Settlement agreements can be presented to employees for various reasons, including a real or alleged redundancy situation or even an agreed exit before or during a disciplinary process. An agreed exit might also come about because you feel you have been badly treated or where your employer, for whatever reason, wants to remove you from your post quickly and with minimum disruption to their organisation or business.

Although either party can make the first move and suggest that an exit package be agreed, employees are often left wondering what their options are. This article will remove the mystery surrounding the negotiation discussions and highlight what negotiating strength employees can hold and what the advantages to agreeing a settlement could be.

Pre-termination discussions

Any discussions about an agreed exit are usually held as a protected conversation or, if there is an existing dispute, on a ‘without prejudice’ basis. In both cases, this means the discussion is private (subject to some limited exceptions) and shouldn’t get raised in any future court or tribunal. You do not have to engage in these discussions if you would prefer not to but they can enable both sides to talk freely about the problems and find a way forward.

As these exit discussions are usually private, if you have a concern about how you have been treated at work (and / or fear no exit will be agreed) you should also raise a formal grievance in accordance with your organisation’s Grievance Policy.

What is a settlement agreement (formally known as a compromise agreement)?

A settlement agreement is a legal document that, once signed, waives any claims or rights of action (usually with a few specific exceptions such as latent personal injury and pension right claims) you may have to sue your employer and any other parties named in the agreement like group companies or the employer’s officers or employees.

In return for this waiver, the employer usually pays you (the employee) a sum of money and/or gives you some other benefit – like an agreed reference, letting you keep items of company property, or releasing you from certain post-termination contractual restrictions.

The agreement will often contain other terms to control the exit and protect the employer, like confidentiality clauses and specific warranties for you to sign. It should also specify a termination date, if it is envisaged that your employment is to come to an end.

So, you’ve had an offer or you think you want to make one. What should you be thinking about?

In summary you should:

- Take time to think about what you want. If your employer has made an offer to you, you should expect to have at least ten days to consider it. Don’t be rushed into making a decision. If you want to make an offer to your employer, consider how best to approach that and what arguments you may be able to put forward.

- Take legal advice from an experienced employment lawyer so you know the strength and value of any likely claims you may have.

- Consider what other leverage you have. Do you have something your employer needs like: personal ownership of any intellectual property rights; a project that needs completing; or an important connection with a client? Offering to co-operate on these may help the negotiation and get a better result.

- Find your employment contract. This should set out your contractual entitlement to notice. In summary, your statutory minimum entitlement to notice is one week for each full year of service up to a maximum of 12 weeks for 12 years plus of a period of continuous employment, but you could be entitled to more notice under your contract of employment. If the notice period under your contract of employment is less, then your statutory rights to minimum notice override this.

- Check your holiday entitlement. Are you going to be owed some holiday or are you going to owe some holiday? Are any other monies or benefits owed?

- Consider the tax implications of any exit payment (including lump sum pension contributions). Take specialist advice if necessary.

- Be aware of any post termination restrictions you have. Many employment contracts will place restrictions on what you can do after your employment ends. Do you need to be released from those as part of the deal?

- Finally, plan any agreed announcement and reference as part of the deal negotiations and don’t tell anyone about your discussions with your employer (other than very close family or as permitted by the terms of the agreement) while you are negotiating.

Chris Morse, a Legal Executive within the Employment team talks through some of the key issues and what you should be considering on an agreed exit or settlement agreement in this video.

What benefits are there if you agree to a settlement agreement?

This is likely to be highly dependent on your individual situation and the reasons for leaving employment.

Settlement agreements are often a preferrable route for employers because you sign away your rights to bring a claim in the employment tribunal. It will often save an employer the time and expense of completing a formal process (for example: redundancy consultation or a disciplinary or grievance procedure) but also gives confidence that you can’t bring a claim in the future.

When deciding on whether to accept the terms of the settlement, it is therefore important to consider if you want to bring a claim and assess the strength of the claim with the support of a legal adviser. If you have strong claims, you may feel that you want the public accountability pursuing them could bring. However, litigation is very costly, as well as emotionally draining, and if you seek a swift resolution without a costly, long and emotional tribunal process, settlement agreements could then be preferrable.

Aside from avoiding a tribunal process, settlement agreements can also benefit you by:

- Reducing legal costs. Employers will usually contribute at least something to obtaining advice you need on the settlement agreement and that contribution can often be negotiated too. You could therefore obtain a good settlement without incurring substantial legal costs.

- Giving greater flexibility on the terms and nature of your exit. You have the ability to propose amendments and additions to the settlement to make the offer more favourable and appealing.

- Resulting in a payment above your contractual or statutory entitlements and allowing you to benefit from some tax efficiencies.

- Securing an agreed reference and announcement which your employer would be legally bound to comply with, thus providing you with certainty on what information will be provided to future employers.

What if you don’t agree with the offer or the terms of the settlement agreement?

If you are unhappy with the offer presented, remember that this is an initial offer and you can seek to negotiate with your employer for better terms. You can progress this yourself before obtaining the necessary legal advice, but you can also negotiate with the support of your legal advisor, who can also provide additional insight on the terms presented and the best strategy to adopt to get the outcome you want.

Although employers cannot be ‘forced’ to improve the proposed terms, our team can support you in presenting arguments for better terms or can do this directly on your behalf with your employer.

As set out above, beneficial changes can be tailored to your circumstances and could vary from negotiating an increase to any termination payment offered to inserting clauses to ensure that your employer pays for the early termination of your company car lease.

When negotiating an agreement it is important to bear in mind that your employer could refuse to negotiate and even retract their offer. Until a settlement agreement is signed, it can be withdrawn. An employer retracting an offer is very rare but it is a risk to bear in mind and one a legal advisor can help you evaluate.

Taking legal advice – what should you expect?

As a settlement agreement involves you surrendering your rights to make future claims, you need this counter-signed by a relevant independent adviser – a definition that includes qualified lawyers. These are extremely important documents and it is important that you take proper specialist advice. Your employer should pay a contribution to your legal fees in this regard to reduce the cost to you – often so that you have no liability for legal costs. If the offered contribution will not be sufficient to cover your costs, your advisor should make you aware of that from the outset.

If your employer has set a date by which the Agreement is to be signed, do let your advisor know. It will also be helpful for them to see a copy of your contract of employment, if you have one.

In discussing the agreement with your legal advisor you should be given the opportunity to fully explain the circumstances leading up to your proposed exit. Your legal advisor should explore with you whether you believe the reasons presented by your employer for terminating your employment are genuine or whether you believe there is an ulterior motive – for example because of your age or because you are pregnant.

Once the background situation has been explored the legal advisor should advise you as to whether you have any likely claims for which you would be waiving your rights.

If you wish to go ahead with the settlement agreement then your legal advisor will go through the terms to ensure that you understand what you are entering into and the obligations on you and your employer.

What if you still don’t want to sign the settlement agreement?

If you already know you don’t want to sign the agreement or you decide after taking advice that you don’t wish to, there is absolutely no obligation for you to do so.

Do be aware that if a settlement agreement is not signed, your employer will not pay a contribution to your legal fees and you would need to pay them yourself. Do discuss this with your advisor if you have any concerns in this regard. Please contact our Employment team if you have any questions regarding settlement agreements.